In California, the cannabis excise tax is set at 15% of gross receipts from licensed retail cannabis sales in California.

Cal NORML spearheaded an effort to roll back the tax from 19% in 2025, but more reform is needed. That rollback will expire on July 1, 2028 unless further action is taken.

Cannabis is heavily overtaxed relative to comparable goods in California.

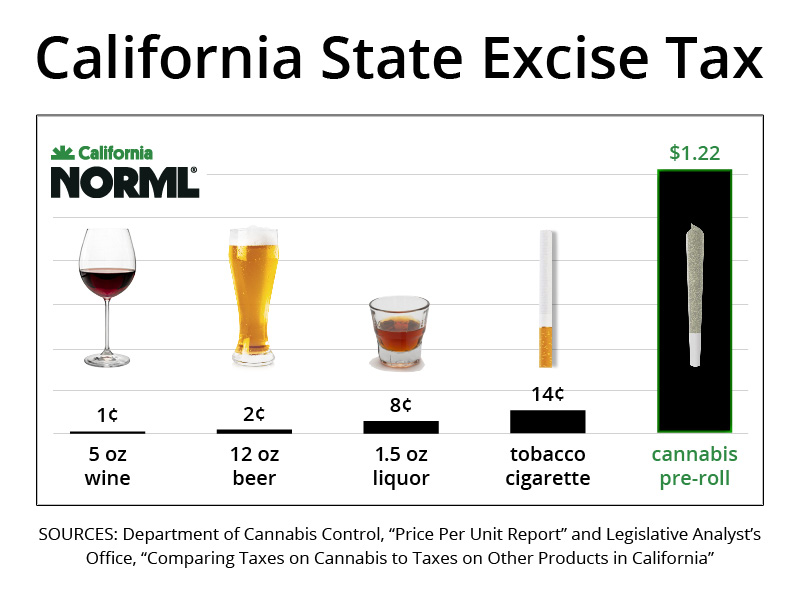

According to the state legislative analyst’s office, state excise tax on a glass of wine is one cent, and on a 12-oz. beer is two cents. For a glass of liquor, the tax is eight cents, and for a tobacco cigarette, it’s fourteen cents.

By contrast, the state excise tax on a cannabis pre-roll is a whopping $1.22. See chart.

Many local governments impose additional taxes on cannabis, ranging as high as 10% in some jurisdictions, including Los Angeles.

There were a total of 239 marijuana tax measures in California from 2009 to 2024. Of those, 86 percent were approved (206 measures).

Excise and local taxes on cannabis are doubly taxed, since they are also subject to sales tax.

Retailers are required to include state and local excise taxes in the definition of “gross receipts” when charging additional sales taxes of 7.25 – 10.5% (on everyone except medical cannabis ID card holders). CDTFA Released a Video clarifying that Local Cannabis Taxes, Delivery Fees, Packaging Fees, etc. all count as gross receipts for the purposes of charging 15% state excise tax.

A bill, SB 1059 (Bradford) to end including excise taxes in the local tax calculations, passed with the support of Cal NORML and its members in 2024. An earlier bill to also stop double taxation at the state level failed.

Adding in state sales tax and local taxes, cannabis products are taxed at a rate as high as 38% (44% if delivered) in California.

Tax and compliance costs get passed onto consumers. Illicit cannabis operations are not subject to the taxes and compliance costs faced by their licensed counterparts and often offer lower prices to consumers on products that are untested and can be misleadingly labeled.

Cannabis taxes currently contribute more to California’s coffers than do alcohol taxes, despite far less sales.

Gov. Newsom’s 2023/24 budget estimated an income of $440 million from alcohol excise taxes. By contrast, state excise taxes on cannabis brought in $624 million in 2023.

California’s excise tax on beer ranked 30th among the 50 states and the District of Columbia, a study from Washington’s Tax Foundation says. A separate report by the same research group found that California’s tax on distilled spirits ranked 40th. Cal Matters’ Dan Walters reported that the liquor industry has been a powerful player that’s helped keep taxes down for years. See: Sure, California is a high tax state — but not when you’re buying beer and whiskey

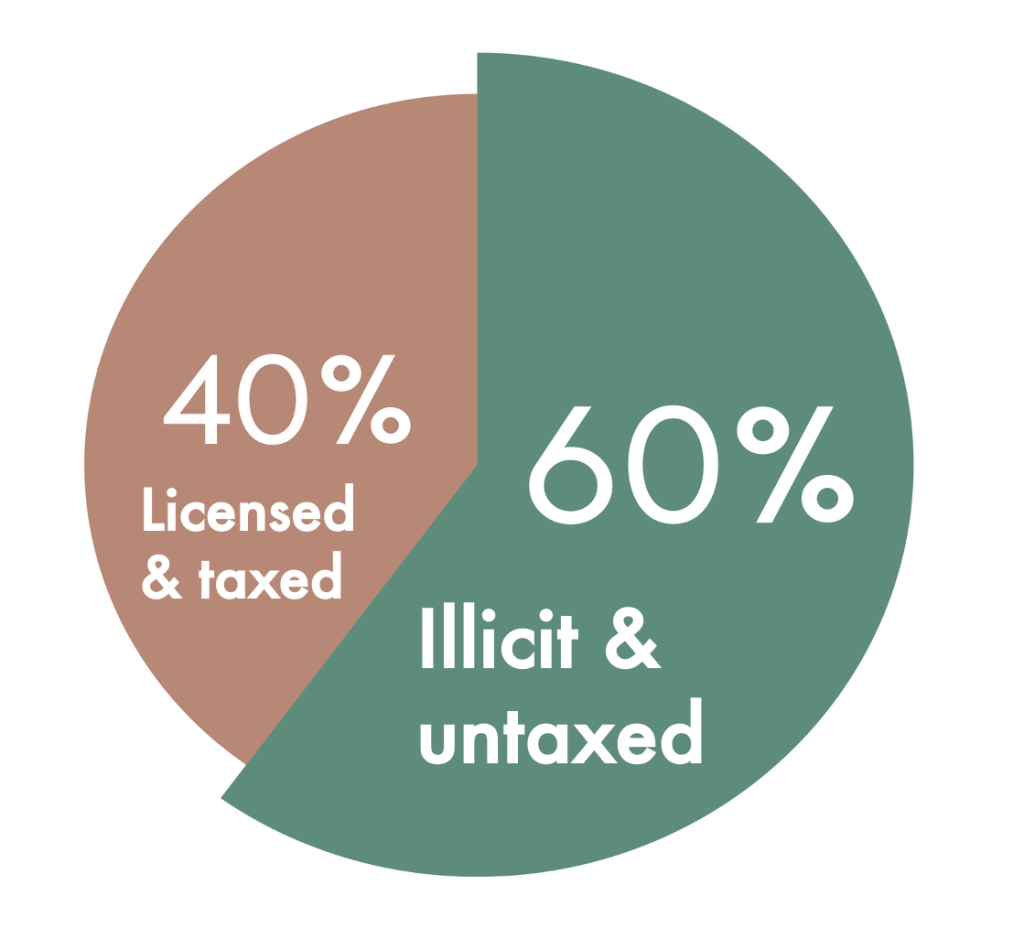

Ten years after legalization, illegal sales continue to account for around two-thirds of marijuana sales in California, according to the Department of Cannabis Control.

Overtaxation of cannabis impedes access to legal, tested, and taxed cannabis for consumers, and fuels the illicit cannabis market while undermining the legal market.

Inactive cannabis licenses are climbing as California companies struggle to stay in business. Inactive licensees don’t make money, or pay taxes. Many of the inactive licenses are equity businesses. California’s licensed retail footprint has flatlined at roughly 1,225 active stores since mid-2023, as 57% of the state’s cities and counties still prohibit cannabis dispensaries, according to the California Department of Cannabis Control (DCC).

If California were on par in per capita sales with states with lower tax rates like Michigan or Montana, it would be generating an estimated $13 billion in annual sales, and the state would be collecting substantially more tax revenue. Instead, the taxable sales for cannabis in 2024 was $4.6 billion. Source.

California’s cannabis consumers want and deserve access to safe, tested, and fairly taxed products.

Some of Prop. 64’s mandates on how cannabis tax monies are allocated will expire in 2028, as will the tax rollback from 19% to 15%. Cal NORML is gearing up for more tax battles in the legislature in 2027.

State Attorney General Rob Bonta has called for lowering the burden. However, at least one powerful group in Sacramento is calling on the government to raise pot tax rates even higher.

Join Cal NORML with a business or personal membership and help us fight for cannabis tax fairness in California.